When you need quick cash to cover an unexpected expense or bridge a financial gap, choosing between payday loans and installment loans can be a critical decision. Both are popular short-term loans, but they differ significantly in terms of repayment, costs, and suitability. This guide explains the key differences to help you make an informed choice, no matter where you are in the world.

Understanding Payday Loans and Installment Loans

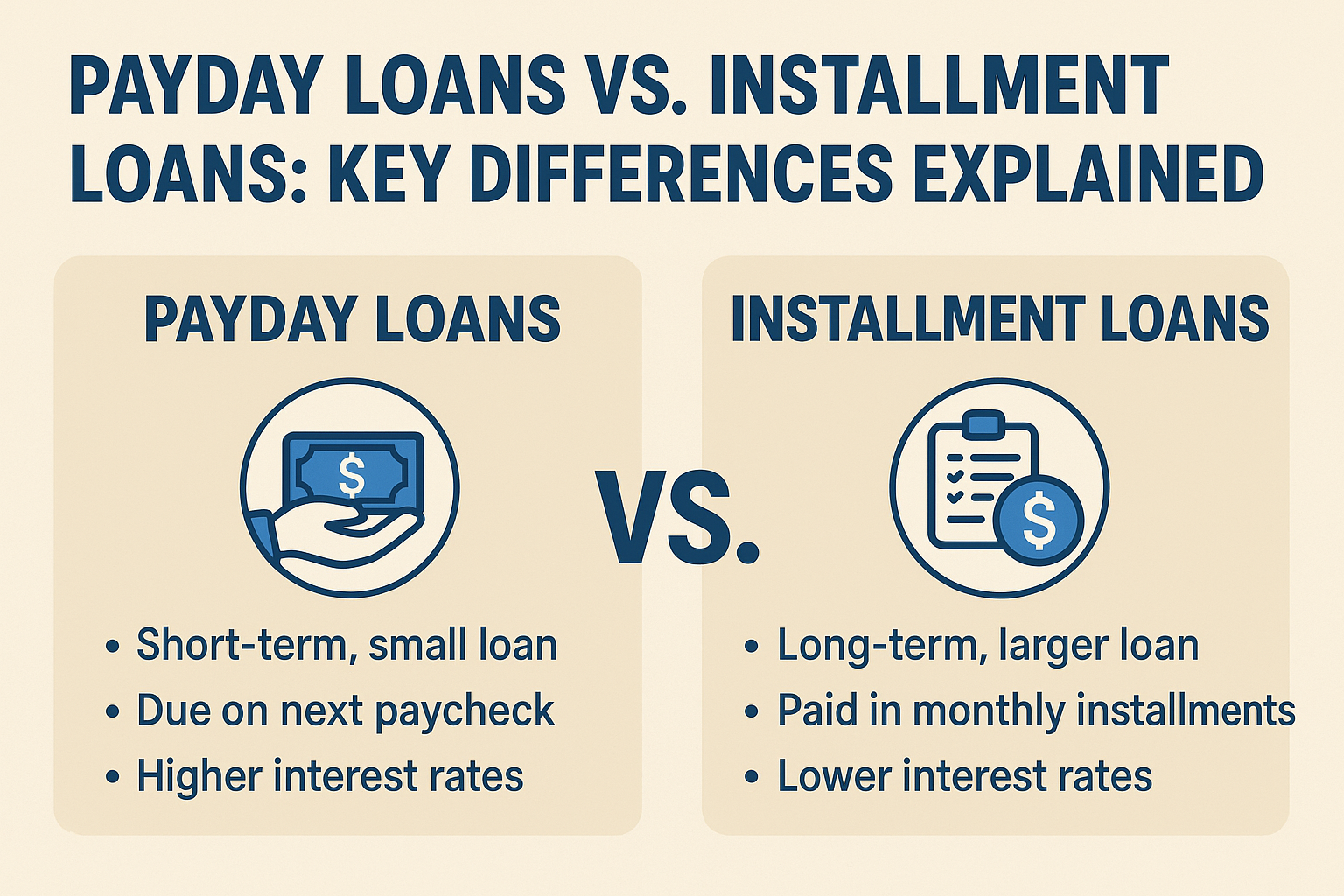

What Are Payday Loans?

Payday loans are small, short-term loans designed to cover immediate expenses until your next paycheck. Typically, they’re due in full within a few weeks, often aligning with your pay cycle. These loans are usually unsecured and require minimal documentation, making them accessible but costly.

Key Features of Payday Loans:

- Small Loan Amounts: Usually limited to smaller sums, ideal for minor emergencies.

- Short Repayment Period: Due in one lump sum, often within 2–4 weeks.

- High Interest Rates: Interest rates or fees can be extremely high, making them expensive if not repaid quickly.

- Easy Approval: Minimal credit checks, suitable for those with lower credit scores.

What Are Installment Loans?

Installment loans allow you to borrow a larger amount and repay it over time in fixed monthly payments. These loans can be used for various purposes, from covering emergencies to funding larger purchases, and typically have longer repayment terms than payday loans.

Key Features of Installment Loans:

- Larger Loan Amounts: Suitable for bigger expenses like medical bills or home repairs.

- Longer Repayment Terms: Repaid over months or years, reducing monthly payment pressure.

- Lower Interest Rates: Generally lower rates than payday loans, though still higher than traditional bank loans.

- Credit Checks: May require better credit for approval, depending on the lender.

Comparing Payday Loans and Installment Loans

To choose the right option, let’s compare payday loans and installment loans across key factors like cost, repayment, accessibility, and use cases.

1. Interest Rates and Costs

Payday Loans: Known for extremely high interest rates or fees, often expressed as a flat fee per borrowed amount. These costs can make repayment challenging if you can’t pay off the loan quickly.

Installment Loans: Typically have lower interest rates than payday loans, spread over a longer period, which reduces the overall cost per payment. However, some may include origination fees or penalties.

Better Option: Installment loans are generally more affordable for larger amounts or longer repayment needs. Payday loans may work for very small, short-term needs if repaid promptly.

2. Repayment Structure

Payday Loans: Require full repayment in a single payment, which can strain your budget if your next paycheck is already allocated. Rolling over or extending the loan often incurs additional fees.

Installment Loans: Offer fixed monthly payments over an extended period, making budgeting easier and reducing the risk of default.

Better Option: Installment loans are better for manageable repayment plans. Payday loans suit those who can repay in full quickly.

3. Loan Amount and Accessibility

Payday Loans: Provide smaller amounts, often capped at a modest sum. They’re easier to obtain due to minimal credit requirements, making them accessible for those with poor credit.

Installment Loans: Allow borrowing larger amounts, but approval may depend on credit history or income verification, which can be a barrier for some.

Better Option: Payday loans are better for quick, small cash needs with minimal requirements. Installment loans suit larger, planned expenses.

4. Use Cases

Payday Loans:

- Urgent, small expenses (e.g., car repairs, utility bills).

- Temporary cash flow shortages before your next paycheck.

- Situations where you’re confident in repaying quickly.

Installment Loans:

- Larger expenses (e.g., medical bills, home improvements).

- Debt consolidation to combine multiple high-interest debts.

- Longer-term financial needs with manageable payments.

Better Option: Choose payday loans for immediate, small-scale needs. Opt for installment loans for bigger expenses or structured repayment.

5. Impact on Financial Health

Payday Loans: Risky if not repaid on time, as high fees can lead to a debt cycle. Timely repayment has minimal impact on credit, as many lenders don’t report to credit bureaus.

Installment Loans: Responsible repayment can improve your credit score, as many lenders report to credit bureaus. Missed payments, however, can harm your credit.

Better Option: Installment loans are safer for long-term financial health if managed well. Payday loans require caution to avoid debt traps.

Pros and Cons at a Glance

| Feature | Payday Loan | Installment Loan |

|---|---|---|

| Interest Rates | Very high, often flat fees | Lower, spread over time |

| Repayment | Single payment, short-term | Fixed monthly payments |

| Loan Amount | Smaller amounts | Larger amounts |

| Accessibility | Easy, minimal requirements | May require credit checks |

| Best For | Small, urgent expenses | Large expenses, debt consolidation |

How to Choose the Right Loan for You

To decide between payday loans and installment loans, consider these questions:

- How much money do you need? Payday loans are better for small, urgent needs, while installment loans suit larger expenses.

- How quickly can you repay? If you can repay in a few weeks, a payday loan might work. For longer repayment, choose an installment loan.

- What’s your credit profile? Payday loans are easier to get with poor credit, while installment loans may offer better terms with good credit.

- Can you avoid a debt cycle? Payday loans can trap you in debt if not repaid quickly, while installment loans offer more manageable payments.

Tips for Borrowing Smartly

For Payday Loans:

- Only borrow what you can repay by the due date.

- Compare lenders to find the lowest fees.

- Avoid rolling over loans to prevent extra costs.

For Installment Loans:

- Shop around for the best interest rates and terms.

- Ensure monthly payments fit your budget.

- Check if the lender reports to credit bureaus to build credit.

Conclusion

Both payday loans and installment loans serve distinct purposes in addressing financial needs. Payday loans are best for small, urgent expenses with quick repayment, but their high interest rates demand caution. Installment loans are smarter for larger expenses or debt consolidation, offering lower rates and manageable payments over time. Evaluate your financial situation, repayment ability, and borrowing needs to choose the option that aligns with your goals and avoids unnecessary costs.